Flooding is one the most devastating and costly natural disasters. Flooding can cause widespread destruction of entire communities at its worst. Even if flooding only affects one home, it can have a devastating financial impact. This is especially true because standard homeowners’ insurance excludes flood coverage.

Separate flood insurance policies can be purchased to help homeowners and renters in the aftermath of a flood. We have compiled some important facts about flood insurance to help you understand flood coverage, how it works, and whether it is necessary.

Flood insurance facts for 2021

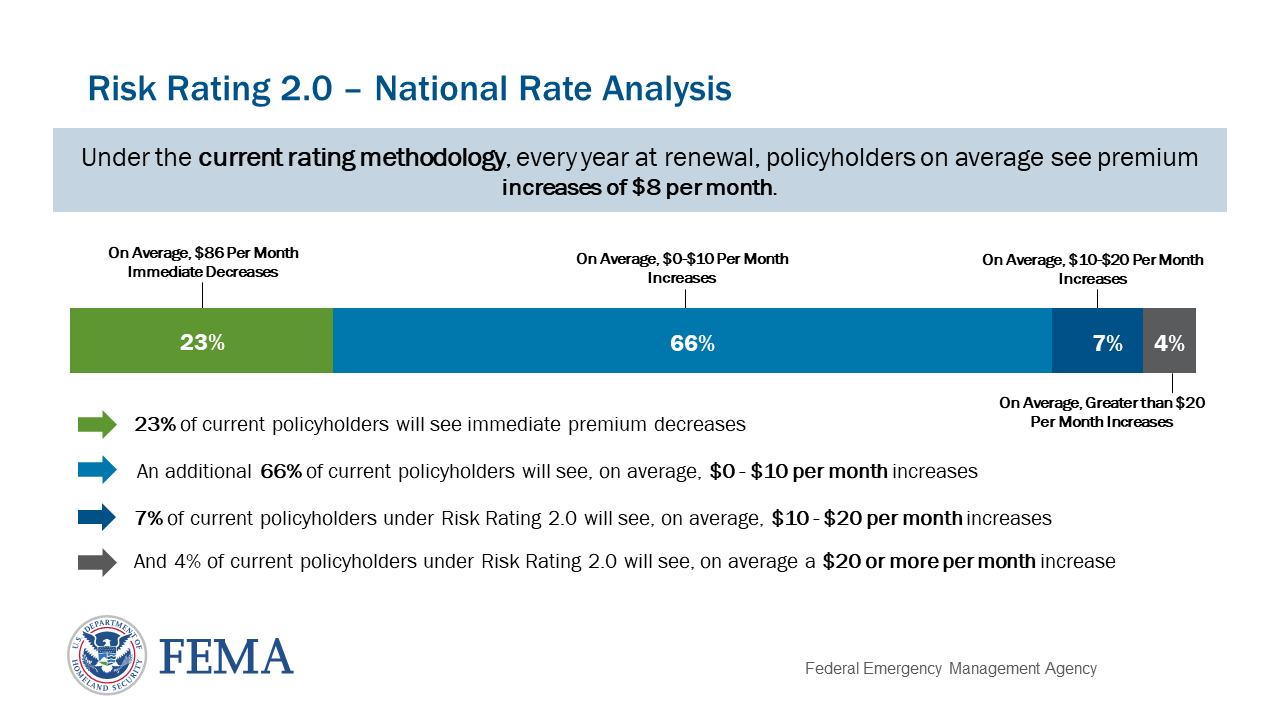

FEMA has a new rating system for flood insurance. Flood insurance policies are backed mostly by FEMA’s National Flood Insurance Program. This new rating system will have a direct impact on what you pay.

This new system, Risk Rating 2.0 is a departure from the traditional risk assessment model that looks at your home’s position on a map. Rates were previously determined by the elevation of your home and its location within the National Flood Map. Risk Rating 2.0 takes a wider range of factors into account, including FEMA’s most recent catastrophe models, advances in actuarial science, and the cost to rebuild your house.

Any new policies created after October 1st will be subject to Risk Rating 2.0. All existing policies will be required to use this rating method starting April 1, 2022. FEMA expects that this new system will reduce flood insurance rates for low-cost homes and do the opposite for high-cost properties. FEMA also predicts that 23 per cent of policyholders would see their rates drop immediately under Risk Rating 2.0.

{kind=link}

What are the consequences of flooding?

You might now have some information about flood insurance and be able to decide if you need this policy type. Here are some facts about flooding and how it can affect lives.

Floods can be very destructive.

Floods are among the most costly natural disasters. Floods can cause serious damage to your home, including the need for furniture replacement and mold remediation. Here are some estimates based on the type of home and water level.

Floods are dangerous

Floods can cause costly damage, but that is not the only danger. Floods can also cause flooding to spread throughout entire communities, and even lead to death. Flood danger can be unpredictable. Although Texas and Kentucky are the states with the highest number of flood incidents, flooding can occur anywhere in the country. This includes landlocked states like Missouri, Virginia, and coastal states like Texas. It is important to remember that floods in a state with low numbers of flood events does not automatically mean they are inexpensive. While Wyoming, North Dakota, and Oregon had low annual flood events, they were high in insurance claims payments.

Check out the flood risk level for your state.

What is Flood Insurance?

Flood insurance is meant to cover damage to your home after a flood and usually costs around $700 per year. Costs vary from one state to the next. Rates will change as FEMA launches Risk 2.0 in October 2021. Flood insurance is an essential part of homeowners’ and renters’ coverage. Renters and homeowners insurance almost never cover flooding.

Flood insurance policies are usually backed by FEMA. They can be purchased through the NFIP. However, you can also buy flood insurance through a private insurance company. Our guide will help you learn more about flood insurance.

Flood insurance is similar to other types of insurance. It pays for any expenses that you incur if a flood event damages your home or property.

What flood insurance covers?

Flood insurance typically covers your home and personal possessions, provided you have both dwelling and personal property coverage (also known as contents). These are the most common items that are covered by flood insurance:

- The structure of your house, including its foundation

- The HVAC, plumbing and electrical systems are all included.

- Flooring

- Appliances

- Furniture

- Electronics

- Clothing

- Window coverings

Flood insurance, just like homeowners insurance may also cover art and rugs, but the payout is often limited.

How do floods damage homes?

Although a little water might not seem to be a big concern, even one inch of water can cause damage that could cost you thousands of dollars. Why is this so? These are some ways floods can cause damage to your home:

- Flood damage: Floodwaters can cause damage to your flooring and weaken the foundation. Flooding can also lead to drywall damage and other structural problems.

- Broken appliances: Most appliances are not built to withstand water exposure. Floods can cause damage to everything, from your oven to fridge to washer and dryer to your washer.

- Problems with your electrical system: Water can cause problems in your home’s electric system. Power surges can damage any plug-ins or wiring that has been damaged by damaged wiring.

- Floodwaters can cause problems with your septic tank: When floodwaters wash into your septic system, it can become clogged.

- Water contamination: Flooding can also lead to water contamination.

- Flood damage to household electronics: A flood could cause many of your household electronics to be damaged. You may also need to worry about mold and mildew if your clothes and furniture are left exposed to water for a prolonged period.

Floods and mold

Mold can quickly grow on damp surfaces after flooding. It can begin as early as 24 hours after being exposed to water. You should dry out your home immediately after the flood to prevent mold growth. If your flood insurance provider believes that you could have prevented the mold growth by taking the appropriate steps after a flood, they won’t cover the cost for mold remediation.

Facts about how to lower your flood risk

There are some things you can do to protect your home from water damage, even if it is located in a floodplain. You may also be able to get flood insurance at a lower price.

- Elevate your property. This will not be an issue if your home is already constructed. If you are considering a new build, consider raising the elevation at which your home is built or building at the highest point of your property.

- You should elevate your utilities. Flood insurance is more expensive if you have utilities that are below the BFE (basis flood elevation), the highest point at which floodwaters would likely rise. You can move electrical panels, water heaters and other utilities to the attic, or on an elevated platform.

- Flood openings are installed: If the water level rises inside your home, flood openings allow water flow out. They prevent water from standing in your home, which can help minimize mold damage. Unless they are flood-openings, doors and windows will not be counted as flood openings by the NFIP.

- Fill in your crawlspace or basement: Generally speaking, if your basement is below BFE, either the NFIP won’t cover it or you will have to pay up to 20% more for flood insurance.

What is an elevation certificate?

The NFIP may require that you obtain an elevation certificate to measure flood risk at your home.

An elevation certificate measures your home’s elevation against the surrounding area. It identifies features such as the lowest floor elevation and other factors that may increase your risk of flooding.

The most important thing is to understand the flood risk in your apartment or home and to purchase flood insurance.